What happened

Applied Aerospace & Defense Group completed its initial public offering on the New York Stock Exchange this week, raising $650 million in gross proceeds. The company provides integrated machining and electronic assembly services for aerospace and military space applications, specializing in high-precision components that require tight tolerances and advanced metallurgy.

The capital will fund expansion at existing facilities in California and Texas. Applied Aerospace cited sustained demand for domestically sourced defense components and space launch hardware as the driver for the buildout. The company did not disclose specific capacity targets or timeline, but the scale of the raise suggests substantial equipment investment and headcount growth.

Public filings show Applied Aerospace's revenue grew 47 percent year-over-year in 2025, reaching $890 million. The company serves prime contractors including Lockheed Martin, Northrop Grumman, and SpaceX, with contracts spanning satellite structures, missile guidance housings, and propulsion system components.

The pricing of the IPO is also worth noting. Applied Aerospace sold its shares at the very top of its target range. This shows that investors are highly eager to back defense manufacturing. The company has a strong backlog of orders, which means its revenue is stable for the next several years. The $650 million in new cash will allow them to buy land and build new factory floors quickly. They plan to buy advanced multi-axis milling centers and automated welding machines to speed up production.

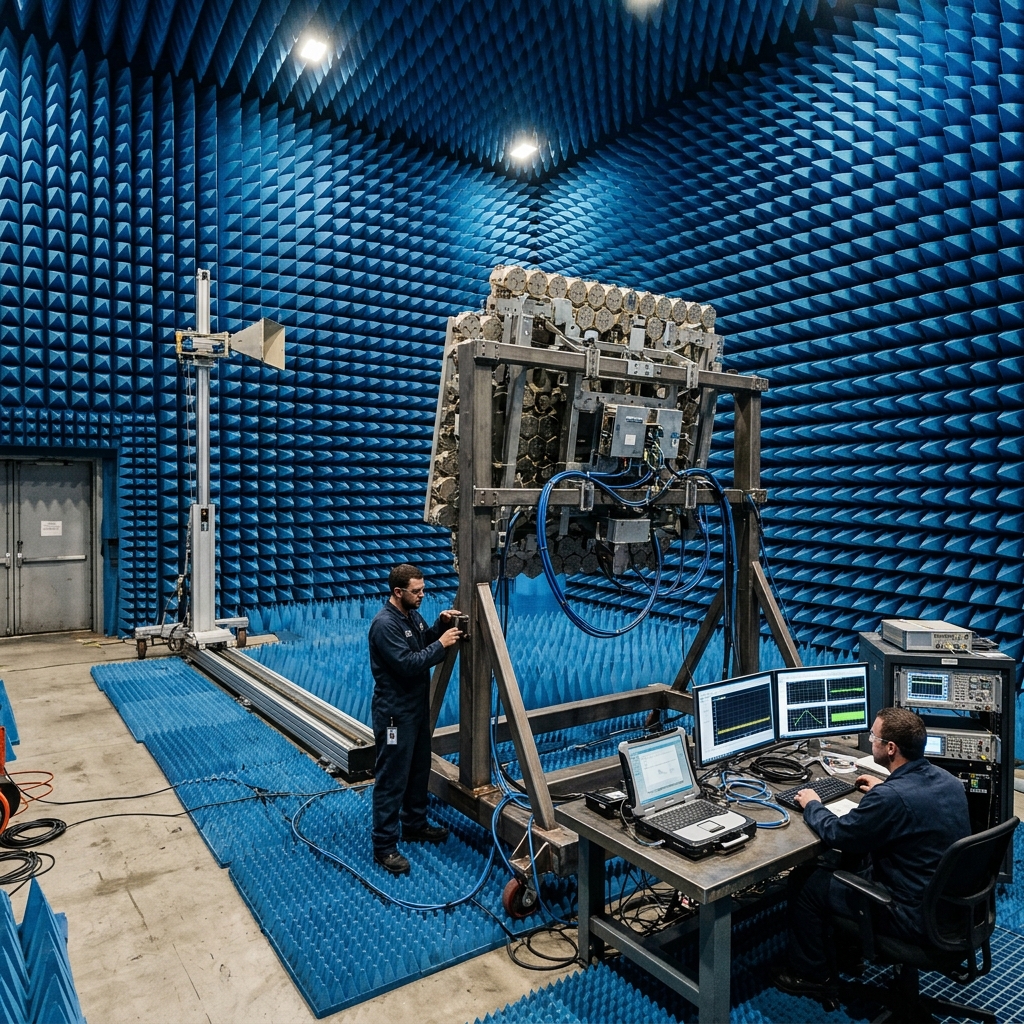

The materials used in space launch and defense systems are highly demanding. These parts are often made from tough metals like titanium, Inconel, and specialized aluminum alloys. Slicing and shaping these metals requires heavy-duty CNC machines. It also requires advanced coolant systems to prevent the tools from overheating. If a tool gets too hot, it can wear out quickly or ruin the part. Applied Aerospace will use a large portion of the new funds to buy these high-end machines and tooling systems.

Why it matters for manufacturers

This IPO is a signal about where the real constraints are in defense manufacturing. Applied Aerospace isn't raising money to design new products or acquire competitors — it's buying machines and floor space. That tells you the bottleneck isn't innovation or market access. It's capacity to cut metal and assemble systems to spec.

For shops already working in defense machining, this validates what everyone's been seeing on the floor: lead times stretching, RFQs arriving with tighter delivery windows, and primes willing to pay premiums for domestic sources with documented quality systems. When a company can raise $650 million based on a thesis of "we'll make more of what we already make," it means the market believes that shortage is structural, not cyclical.

The focus on California and Texas is deliberate. Both states have concentrations of aerospace primes and emerging space launch providers. Proximity matters when you're shipping high-value components that require hand-carry logistics or when engineering changes need same-day collaboration. Applied Aerospace is betting that co-location with customers justifies the higher operating costs in those regions.

What's less clear is whether this expansion addresses the skilled labor problem. Precision machining for defense requires machinists who can interpret GD&T callouts, program five-axis mills, and understand material certifications. You can't hire those skills off the street, and training timelines run six to eighteen months depending on complexity. Applied Aerospace's ability to staff new capacity will determine whether this $650 million translates into actual throughput or just expensive idle equipment.

The IPO also highlights a competitive dynamic smaller shops should watch. Large, well-capitalized manufacturers can now access public markets to fund expansion at a scale that crowds out competitors. If Applied Aerospace adds capacity faster than demand grows, pricing pressure could ripple through the supply base. But if demand continues to outpace even aggressive buildouts, there's room for multiple players — including contract manufacturers who can meet the same standards for CMM inspection and quality assurance.

To meet the tight tolerances of defense parts, shops must use advanced quality systems. GD&T (Geometric Dimensioning and Tolerancing) is a system of symbols used to define the exact shape and size of a part. In defense work, tolerances are often measured in microns. If a guidance fin or sensor mount is off by a tiny fraction, the missile or satellite will not function. This is why CMM (Coordinate Measuring Machine) inspection is so important. Every part must be checked and documented. RivCut operates these advanced inspection systems daily, and we know how critical they are for winning defense contracts.

What to watch next

Track whether Applied Aerospace can deliver capacity on the timeline investors expect. Public companies report quarterly, so we'll see within a year whether equipment installations are hitting targets and whether new hires are ramping production or sitting through extended training.

Also watch for follow-on moves from competitors. If other mid-tier defense manufacturers pursue similar raises or announce expansions, it confirms this isn't just one company's bet — it's an industry-wide capacity sprint. That would pressure smaller shops to either invest in their own capabilities or risk getting squeezed out of long-term agreements.

Finally, pay attention to how primes respond. If Lockheed or Northrop start announcing multi-year supply agreements with Applied Aerospace, that's a sign they're locking in capacity early. For independent shops, that could mean fewer opportunities with primes but more potential subcontract work as Applied Aerospace itself needs to outsource overflow or non-core operations.

The defense manufacturing base is reconfiguring in real time. Capital is flowing to companies that can prove they can scale precision work domestically. Whether you're competing with that or positioning to supply into it depends on how fast you can adapt your own capabilities.

Another area to watch is subcontracting. As Applied Aerospace grows, they will likely focus on large assemblies and integration. This means they will need to outsource smaller components to secondary shops. For smaller contract machine shops, this expansion could lead to new business. Sourcing managers should look at this secondary tier of suppliers to find capacity. If you cannot get a slot with a large supplier like Applied Aerospace, a smaller, high-quality contract shop might be a better choice.

We should also monitor defense budgets. The demand for these parts is driven by government contracts. If geopolitical tensions remain high, defense spending will likely grow. This will support the growth of companies like Applied Aerospace. But if budgets are frozen or cut, the industry will face overcapacity. Watch if Applied Aerospace tries to diversify into commercial markets, like communications satellites or medical equipment, to reduce their risk.

Frequently Asked Questions

Why did Applied Aerospace & Defense Group launch an initial public offering (IPO)?

The company launched its IPO to raise $650 million in gross proceeds to fund the expansion of its precision manufacturing facilities in California and Texas. This expansion will help meet the growing demand for domestically sourced defense components and space launch hardware.

What types of products does Applied Aerospace manufacture?

Applied Aerospace specializes in high-precision machined components and integrated electronic assemblies. These parts are used in critical aerospace and military space applications, such as satellite structures, missile guidance housings, and rocket propulsion systems.

Why is domestic precision manufacturing capacity a bottleneck in defense?

The bottleneck is not design or technology, but the physical capacity to cut metal and assemble components to strict military specifications. The supply chain is stretched, and prime contractors are facing long lead times for complex parts due to a shortage of U.S. machine shops.

What role does skilled labor play in the success of this expansion?

Skilled labor is the most critical factor. Operating advanced multi-axis CNC machines and performing quality inspections requires highly trained machinists and technicians. Applied Aerospace must invest heavily in training and recruitment to ensure its new equipment does not sit idle.

When a company raises $650 million to make more of what it already makes, the bottleneck isn't innovation — it's capacity to cut metal to spec.