What happened

Automakers built battery plants for an EV boom that has not arrived on schedule. Now they are trying to pivot those facilities toward stationary energy storage to keep production lines running. Reuters reports the shift is neither cheap nor straightforward. Furthermore, demand for grid-scale storage is not growing fast enough to absorb the glut of unused EV battery capacity.

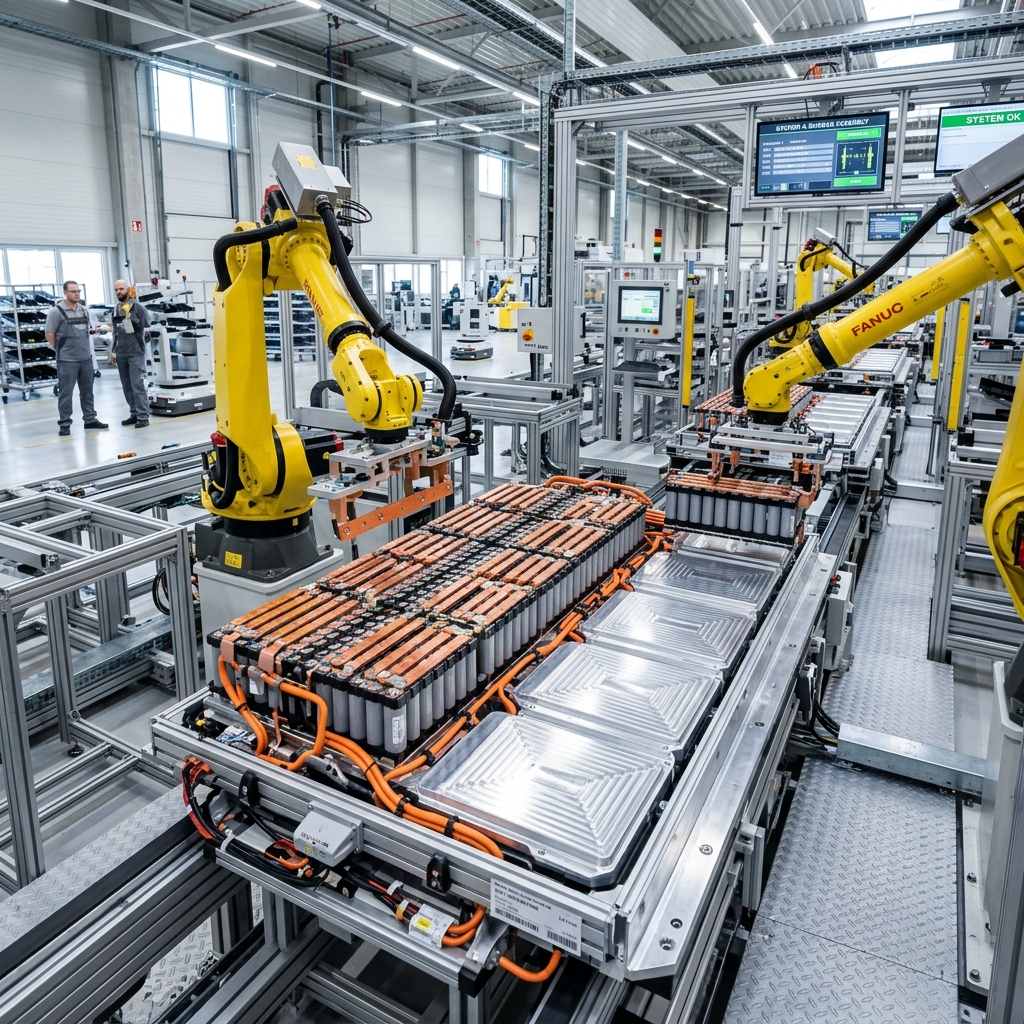

The mismatch comes from overbuilding. Between 2022 and 2025, battery factories expanded quickly. Global capacity grew by sixty percent. This was based on high growth forecasts. But electric car sales slowed down. In the United States and Europe, sales growth dropped to single digits. This left automakers with massive factories they did not need. These factories were set up to make automotive cells. These cells are designed for high energy density. They are meant to fit in cars. They do not work well for power grids without major changes.

Retooling a battery assembly line is very hard. It is not a simple software update. You cannot just change the settings on a machine. Automakers must buy new equipment. They need different coating systems for the chemicals. They need new assembly jigs to hold larger cells. They also need different testing equipment. This machinery is highly specialized. The lead times to buy these machines are very long. It can take six to twelve months to get them. The costs are also huge. Retooling a single production line can cost tens of millions of dollars.

The delay in electric car demand has caused financial pain. Automakers are writing down the value of their plants. This means they are admitting the plants are worth less money. The situation has also strained relationships. Many battery plants are run as joint ventures. Automakers and battery companies are arguing over who pays for the losses. Also, many of these plants received government money. This adds political pressure. Leaders want to keep the factories open to save jobs. Pivoting to grid storage is seen as a way to avoid total failure.

Battery chemistry differences

One of the biggest hurdles is battery chemistry. Electric cars need a lot of power in a small space. This is called energy density. It allows the car to drive a long distance on one charge. To get high density, automakers use NMC chemistry. This stands for nickel, manganese, and cobalt. These batteries are very powerful. But they are also expensive. They have a shorter lifespan. They can also catch fire if they are damaged.

Grid storage systems have different needs. They do not need to be small or light. They sit on the ground in large metal containers. But they must last a long time. They need to charge and discharge thousands of times. For this reason, grid developers prefer LFP chemistry. This stands for lithium iron phosphate. LFP batteries are heavier and have less energy density. But they are much cheaper. They are also safer and last longer.

Switching a factory from NMC to LFP is a major task. The chemical mixing process is different. The materials must be handled with different safety rules. The machines that coat the metal foils must be adjusted. This requires new suppliers for raw materials. It also means workers need new training. The quality control process must be redesigned. All of these changes take time and money.

Why it matters for manufacturers

This situation offers a lesson about capacity planning. Building for a forecast is risky. If you lock in single-purpose machines early, you can get stuck. Automakers are now stuck with expensive assets. They must decide if they want to lose their investment. Or they can spend even more money to chase the grid market. This is a tough choice for any business leader.

The impact trickles down to smaller suppliers. Many machine shops have contracts with automakers. They make parts for electric cars. When EV production slows, their orders get cut. This hurts their business. Sourcing parts for grid storage is an option. But grid storage orders are different. They are smaller and have more variety. Machine shops must adapt. They must be able to handle low-volume production. They cannot rely on long runs of the same part anymore.

The risk of focus is also clear. Sourcing all your business from one application is dangerous. If that application fails, your business fails. Automakers are learning this the hard way. Suppliers must also learn this. They should diversify their customer base. They should not rely only on automotive contracts.

Procurement teams must watch the timing of these changes. Grid storage is growing. The U.S. added a lot of storage capacity last year. But it is still small compared to the car market. If automakers flood the market with storage batteries, prices will drop. This could hurt storage battery companies. But it could also lead to longer lead times. Suppliers may struggle to meet the sudden demand.

What to watch next

We must watch for new corporate structures. Look for joint ventures or spin-offs. If an automaker separates its battery business, it is a sign. It shows they are serious about grid storage. They want to isolate the costs. If they keep the business inside, it may mean they are struggling. They might just be trying to cover up their losses.

We should also monitor utility buying patterns. Power companies buy grid storage. They work on long timelines. They sign big contracts. If they buy more batteries now, it will help. It will absorb the excess supply. But if they slow down, the oversupply will get worse. This would lead to more factory shutdowns.

Finally, keep an eye on trade policy. The government is setting new rules for battery parts. They want to block Chinese materials. This will force companies to find new sources. It will change where batteries are made. New tariffs could make batteries more expensive. Or they could create a protected market for U.S. factories. Suppliers must stay informed about these political shifts. They affect every contract.

Frequently Asked Questions (FAQ)

Why are automakers pivoting EV battery plants to stationary storage?

Answer: Automakers are pivoting because passenger EV sales growth has slowed, leaving battery plants with excess capacity that they hope to use for grid energy storage.

What is the difference between EV batteries and stationary storage batteries?

Answer: EV batteries favor high energy density (NMC chemistry) for range, while stationary storage batteries favor safety, low cost, and long lifespan (LFP chemistry).

What are the main costs associated with retooling a battery factory?

Answer: Retooling costs include buying new chemical coating systems, cell assembly jigs, safety equipment, and testing gear, which can exceed tens of millions of dollars.

How does the battery pivot affect component suppliers?

Answer: Suppliers face delayed EV contracts but gain new opportunities to supply enclosures, brackets, and thermal hardware for storage systems.

Building for a forecast is necessary, but locking in single-purpose tooling before demand materializes creates stranded assets.